Introduction

Health insurance enrollment runs on a fixed calendar. Open enrollment opens, closes, and everyone's locked in. Until life happens. A new baby arrives in March. A job ends in July. A marriage happens in September. None of these wait for November's enrollment window, and the benefits system can't simply ignore them.

That's where qualifying life events (QLEs) come in. They're the mechanism built into federal benefits law that allows individuals to make coverage changes mid-year when a significant personal change alters their insurance needs.

QLEs surface constantly across HR workflows, benefits administration processes, and carrier communications. Yet the specifics which events qualify, how the enrollment window is triggered, what documentation is required are frequently misunderstood by both employees and the platforms serving them.

This guide covers what QLEs are, which life changes count under federal rules, and how the process works from event to enrollment update. It's written specifically for benefits platforms and HR systems that handle these triggers in production.

Key Takeaways

- A qualifying life event (QLE) is a specific personal or family circumstance that allows coverage changes outside the annual Open Enrollment Period.

- QLEs fall into four categories: loss of health coverage, household/family changes, changes in residence, and other IRS/ACA-defined events.

- Each QLE opens a Special Enrollment Period (SEP): 30 days for employer plans, 60 days for ACA Marketplace plans.

- Documentation is required to verify the event; missing the SEP window usually means waiting until the next Open Enrollment.

- For benefits platforms, QLEs are data triggers that must be detected, verified, and synced across HRIS, carrier, and payroll systems immediately.

What Is a Qualifying Life Event?

A qualifying life event is a specific personal or family circumstance recognized under federal regulations (including the ACA, ERISA, and IRS Section 125) that grants an individual the right to change their health insurance coverage outside of the standard Open Enrollment Period.

When a QLE occurs, it activates a Special Enrollment Period (SEP), a defined window during which enrollment changes can be made.

Why QLEs Exist

Health insurance enrollment is restricted to annual windows to prevent adverse selection the tendency of people to enroll primarily when they anticipate needing care, which destabilizes the risk pool. The NAIC defines adverse selection as "the tendency of persons with a higher-than-average chance of loss to seek or maintain insurance to a greater extent than persons with an average or lower-than-average chance of loss."

QLEs are the safety valve. When a major life change genuinely alters someone's coverage needs (a job loss, a new child, a marriage), they aren't left waiting months for the next enrollment window.

What QLEs Are Not

Benefits administrators and platform teams often need to distinguish QLEs from related but separate concepts:

- Open Enrollment is a universal annual window available to everyone, not triggered by a specific event.

- COBRA is a continuation coverage election, a way to maintain existing coverage after a QLE, not a new enrollment right.

- Hardship exemptions apply to marketplace coverage in narrow circumstances and don't function as enrollment triggers.

The Regulatory Landscape

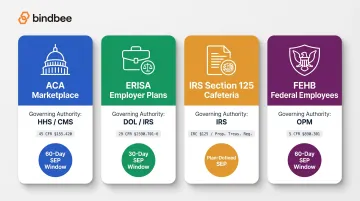

QLEs are governed under three overlapping regulatory frameworks, each with different event lists and rules:

| Framework | Governing Authority | Primary Regulation | SEP Window |

|---|---|---|---|

| ACA Marketplace | HHS/CMS | 45 CFR 155.420 | 60 days |

| ERISA Employer Plans | DOL/IRS | 26 CFR 54.9801-6 | Minimum 30 days |

| IRS Section 125 Cafeteria | IRS | 26 CFR 1.125-4 | Per plan document |

| FEHB (Federal Employees) | OPM | 5 CFR Part 890 | 60 days |

ERISA/HIPAA special enrollment rights set a mandatory floor: plans must honor them. IRS Section 125 is permissive. The regulation states plans "may permit" election changes, not that they're required to. The operative QLE list for any given employer-sponsored plan depends on what that plan document actually allows, creating variation that directly affects which elections employees can make.

Types of Qualifying Life Events

Loss of Health Coverage

This is the most common QLE category. Qualifying events include:

- Job loss and associated loss of employer-sponsored coverage

- Aging off a parent's plan at 26 (required under ACA Section 1001)

- Loss of eligibility for Medicare, Medicaid, or CHIP

- Loss of student health plan coverage

Voluntary cancellation and failure to pay premiums do not qualify. Under 26 CFR 54.9801-6, loss of coverage "due to a failure to pay premiums on a timely basis or for cause" is explicitly excluded as a triggering event. Systems that process loss-of-coverage events must distinguish involuntary from voluntary terminations.

Household and Family Changes

Core events in this category:

- Marriage

- Divorce or legal separation (when it results in coverage loss)

- Birth or adoption of a child

- Death of the primary policyholder

- Court-ordered dependent coverage (such as a child support order)

Newborn and adopted child coverage is retroactive by law, a meaningful exception to standard enrollment timing. The DOL confirms that coverage is "effective retroactive to the date of birth, adoption, or placement for adoption."

This creates a backdated effective date scenario that benefits platforms must handle explicitly. Payroll deductions, carrier EDI feeds, and premium reconciliation all need to account for the gap between the event date and the date the employee submits enrollment.

Changes in Residence

Geography-based events are distinct from family-status changes: a permanent move qualifies for a SEP only if it changes the individual's available plan options, meaning the move takes them to a different county or ZIP code with different Marketplace offerings. Qualifying moves include:

- Moving to a new ZIP code or county that changes available plans

- Moving to the U.S. from a foreign country or territory

- Moving for school or seasonal work

- Moving to or from transitional housing or a shelter

Moving within the same plan service area (where available plans don't change) does not trigger a SEP.

Other Qualifying Events

The ACA Marketplace recognizes a broader set of events beyond the employer-plan framework:

- Gaining U.S. citizenship or lawful presence

- Release from incarceration

- Gaining membership in a federally recognized tribe

- Natural disaster declarations (FEMA-designated)

- Domestic abuse or spousal abandonment

- Becoming newly eligible for premium tax credits

These ACA-only events (citizenship, incarceration release, FEMA declarations) do not appear in IRS Section 125 or ERISA. Benefits platforms supporting both marketplace-eligible populations and employer plan enrollees need to maintain separate event lists mapped to the correct regulatory authority.

How the QLE Process Works

When a qualifying life event occurs, it activates a defined sequence: from the triggering event through documentation, enrollment window, plan selection, and downstream data updates. Each stage carries its own timing requirements.

Triggering the Event

For employer-sponsored plans, the employee typically self-reports the QLE to HR or the benefits administrator via an HRIS portal or benefits platform. For Marketplace plans, the individual reports to the Marketplace directly.

The SEP clock starts from the date of the event, not the date of reporting. This distinction matters operationally. An employee who gets married on June 1 but doesn't report it until June 20 has already consumed 19 days of a 30-day SEP window. Delayed self-reporting is a leading cause of missed SEP windows, and platforms relying on manual reporting workflows are most exposed to this problem.

The Special Enrollment Window

| Plan Type | SEP Window | Clock Starts |

|---|---|---|

| ACA Marketplace | 60 days | Date of triggering event |

| ERISA employer plans | Minimum 30 days | Date of event |

| FEHB | 60 days | Date of qualifying life event |

| Medicaid/CHIP loss | 60 days | Date of coverage loss |

Some employers voluntarily extend their SEP windows beyond the 30-day ERISA minimum. For employees eligible for both employer coverage and Marketplace plans, both clocks run simultaneously from the same event date. Worth flagging when an employee is weighing options.

Missing the window has real consequences. The individual must wait for the next Open Enrollment Period, potentially leaving them or their dependents uninsured or locked into inadequate coverage for months.

Documentation and Verification

To confirm a QLE and process the enrollment change, the employer or Marketplace requires supporting documentation. Common requirements by event type:

| Life Event | Required Document |

|---|---|

| Marriage | Marriage certificate |

| Birth or adoption | Birth certificate or adoption decree |

| Divorce | Divorce decree or legal separation agreement |

| Loss of employer coverage | Termination letter or coverage termination notice |

| Loss of prior coverage | Letter from prior carrier confirming coverage end date |

Documentation standards for employer-sponsored plans are plan-defined, not federally prescribed. The DOL notes that "your plan may require that the notice be in writing," but specific document requirements vary by plan. Documents must typically be submitted within the SEP window to validate the enrollment change.

Coverage Changes and System Updates

Once the QLE is verified, the employee selects a new plan or adjusts their existing coverage adding or removing dependents, changing plan tiers, or switching plans entirely.

The enrollment change then needs to propagate to multiple systems:

- Payroll must update premium deductions to reflect the new plan or dependent configuration

- The carrier needs coverage activation, member record updates, and for terminations, EDI 834 file updates

- FSA/HSA administrators must update if election changes are involved

- COBRA administrators must be notified for loss-of-coverage events

This multi-system update is where integration failures concentrate. An HRIS logging a marital status change doesn't automatically update the benefits enrollment record or notify the carrier. Without real-time data connections, these updates require manual reconciliation, creating compliance risk, coverage gaps, and billing errors. That gap is a structural problem, not an edge case.

What QLEs Mean for Benefits Platforms and HR Systems

Unlike open enrollment (a scheduled, batch-based process), QLEs are asynchronous. They can happen any day of the year, require immediate action, and must trigger coordinated updates across HRIS, benefits administration, payroll, and carrier systems. Platforms that treat QLEs as manual workflows rather than structured data events create exactly the compliance and data gaps that downstream systems can't absorb.

Where Integration Failures Occur

The gap between when a QLE is recorded in a source system and when downstream systems actually reflect the change is where most problems emerge:

- An HRIS records a dependent addition, but the benefits enrollment record isn't updated

- A termination is logged in payroll, but the carrier doesn't receive the change for 30+ days

- A newborn is added retroactively, but payroll continues deducting the prior premium amount for two pay cycles

These aren't edge cases. Before connecting through Bindbee, Clever Benefits relied on SFTP-based CSV transfers between their platform and customers' payroll systems. Data was never truly current, and each transfer required manual intervention. After switching to real-time sync, they covered 50+ employers and eliminated manual deduction entry entirely.

ThrivePass faced a different version of the same problem: batch 834 files created 30-90 day lags between QLE events and system updates, and they frequently missed the federal 14-44 day COBRA notice window. After moving to webhook-based event detection, they cut benefits admin onboarding from 6 weeks to under 1 week and met compliance deadlines consistently.

What Real-Time QLE Infrastructure Requires

For benefits administration platforms and HR Tech builders that need to detect and process life events across multiple employer clients, the core technical requirements are:

- Event detection that identifies QLEs as they occur in source HRIS systems, not on a batch schedule

- Structured event payloads that distinguish between dependent additions, marital status changes, terminations, and other event types

- Retroactive effective date support for birth and adoption events

- Multi-system sync that propagates changes to payroll, carrier, and FSA/HSA systems in a single coordinated update

Bindbee provides webhooks for life events (including new hires, terminations, and dependent changes) alongside real-time eligibility data sync across 65+ HRIS and carrier systems through a single unified API. The result: no reconciliation queue, no stale eligibility data, and no manual handoffs between the moment a QLE occurs and when every downstream system reflects it.

Conclusion

Qualifying life events are a structured mechanism built into federal benefits law, designed so that major personal changes don't strand individuals without appropriate coverage. The rules governing them are specific, the timelines are strict, and the downstream effects touch every connected system in the benefits stack.

For HR professionals, understanding the QLE process means employees get clear guidance before SEP windows close. For benefits platforms and HR Tech builders, it means the infrastructure needs to match the urgency. When a qualifying event fires, the system response needs to be immediate:

- Real-time event detection as status changes hit the HRIS

- Structured event data that downstream systems can act on without manual intervention

- Synchronized updates across payroll, carriers, and enrollment records, not queued for the next batch cycle

Miss any of those, and the SEP window closes before the employee ever sees an enrollment prompt.

Frequently Asked Questions

What is a qualifying event for benefits?

A qualifying event, or qualifying life event, is a specific personal or family circumstance that allows an individual to change their health insurance coverage outside the annual Open Enrollment Period. Common examples include marriage, job loss, and the birth of a child. Each qualifying event triggers a Special Enrollment Period during which changes can be made.

What are common qualifying events for benefits?

The four main categories are: loss of health coverage (job loss, aging off a parent's plan at 26), household changes (marriage, divorce, birth or adoption), changes in residence that alter available plan options, and other IRS/ACA-defined events such as gaining citizenship or leaving incarceration.

What does the IRS consider a qualifying event?

Under IRS Section 125, qualifying events for cafeteria plans and FSAs include marriage, divorce, birth or adoption of a child, death of a dependent, and changes in employment status. This list applies to employer-sponsored pre-tax benefit plans and differs from the broader ACA Marketplace QLE definitions.

Does a qualifying event allow you to change plans?

Yes. A qualifying life event opens a Special Enrollment Period during which an individual can enroll in a new plan, switch plans, add or remove dependents, or drop coverage depending on the nature of the event and the type of plan involved.

How do I prove a qualifying event for benefits?

Documentation requirements vary by event. Common examples include a marriage certificate, birth or adoption certificate, divorce decree, employer termination letter, or a prior carrier's coverage termination notice. Documents must typically be submitted within the Special Enrollment Period window.

What is a qualifying life event for FEHB?

Under the Federal Employees Health Benefits program, QLEs cover the same core events as ERISA-governed employer plans (marriage, divorce, birth or adoption, loss of coverage), but are administered by the U.S. Office of Personnel Management (OPM). OPM sets its own event definitions, including military-specific events not found in private-sector rules. The FEHB SEP window is 60 days from the qualifying event.