Key Takeaways

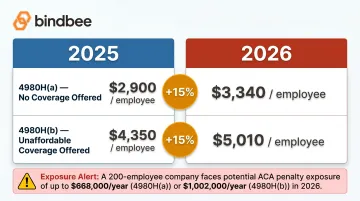

- 2026 ACA penalties increased 15%: $3,340 per employee (4980H(a)) and $5,010 per employee (4980H(b)), the steepest single-year jump in recent cycles

- Quality webinar series cover ALE determination, Pay-or-Play rules, affordability safe harbors, and 1095-C coding, going well beyond surface-level regulatory summaries

- Use on-demand formats for foundational training; schedule live sessions in Q3/Q4 to catch IRS affordability threshold updates as they drop

- ACA "certification" is a voluntary professional credential with no government mandate behind it

- The most common compliance failure is stale or siloed data across HRIS, payroll, and benefits systems

Why ACA Compliance Training Deserves More Than a Once-a-Year Checklist

ACA compliance sits at the intersection of workforce classification, benefits design, and IRS reporting. Every one of those layers moves annually.

The Penalty Math Has Changed

Per IRS Rev. Proc. 2025-26, 2026 penalty amounts are:

| Penalty Type | 2025 Amount | 2026 Amount | Change |

|---|---|---|---|

| 4980H(a): No coverage offered | $2,900/employee | $3,340/employee | +15% |

| 4980H(b): Unaffordable/inadequate coverage | $4,350/employee | $5,010/employee | +15% |

For a mid-size employer with 200 full-time employees, a single 4980H(a) trigger means $668,000 in annual exposure before any dispute process begins. Fisher Phillips has reported that IRS Letter 226-J assessments for some employers run into the millions.

The 4980H(a) and 4980H(b) penalties work differently and it matters:

- 4980H(a) triggers when an ALE fails to offer minimum essential coverage to at least 95% of full-time employees. One missed group can expose the entire workforce count.

- 4980H(b) triggers per employee who receives a premium tax credit on the Exchange, meaning a single misclassified variable-hour worker or incorrect affordability calculation creates individual per-head exposure

Parameters Change Every Year

The affordability threshold has moved three years running:

- 2024: 8.39%

- 2025: 9.02%

- 2026: 9.96%

Each shift resets the math for affordability calculations and safe harbor caps. For 2026 plans, the FPL safe harbor requires employee-only premiums of $129.89 or less per month (lower 48 states), a figure that changes annually and directly affects benefit design decisions made in Q3.

An HR team running open enrollment on last year's materials is working with numbers that are already wrong. A Q1 refresher completed before the IRS releases summer guidance has the same problem: the figures it trained on may be outdated before open enrollment even opens.

What a Quality ACA Compliance Webinar Series Should Cover

A surface-level overview of the ACA differs substantially from a series built for practitioners who apply the rules to real employee populations. The difference shows up fast, usually in how deeply the program covers ALE determination and 1095-C coding.

Foundational Topics Every Series Must Address

A credible series starts with ALE determination. Everything else depends on it:

- Part-time hours aggregated and divided by 120 monthly determines FTE count; the full-time threshold sits at 30 hours/week or 130 hours/month

- Variable-hour and seasonal workers require look-back measurement methods, covering standard measurement, administrative, and stability periods

- Controlled group and affiliated service group rules require employers sharing ownership to aggregate headcount, one of the most commonly missed ALE triggers

From there, the series should cover the three affordability safe harbors with their Form 1095-C Line 16 codes:

| Safe Harbor | Line 16 Code |

|---|---|

| W-2 Wages | 2F |

| Rate of Pay | 2G |

| Federal Poverty Line | 2H |

1095-C Coding Depth

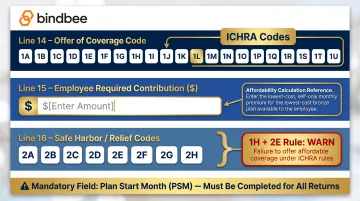

The IRS instructions cover 90+ possible code combinations across Lines 14, 15, and 16. Most webinars don't come close to covering the consequential ones. A practitioner-level series should walk through:

- Line 14 offer codes (1A through 1U), including ICHRA offers (1L–1U) with ZIP-code-based affordability testing

- Line 16 safe harbor and relief codes (2A–2H), with special attention to the rule that 1H must appear on Line 14 whenever 2E is used on Line 16

- The Plan Start Month field is now mandatory on 2024 and 2025 tax year forms and cannot be left blank

Electronic filing obligations deserve their own segment. Since T.D. 9972 reduced the e-filing threshold to 10 aggregate information returns, virtually every ALE now files Forms 1094-C/1095-C through the IRS AIR system, making this a practical necessity, not an edge case.

Advanced Topics Worth Seeking Out

Higher-quality on-demand programs include:

- Multiemployer plan reporting and the 2E relief code

- Self-insured plan reporting under Section 6055 (Part III of Form 1095-C)

- ICHRA design and affordability testing by employee class

- Mid-year qualifying life event handling and offer-of-coverage obligations

- The alternative furnishing method under T.D. 9970 (website posting instead of mailing)

On-Demand vs. Live ACA Webinars: Choosing the Right Format

Choosing between on-demand and live formats determines whether your team gets timely, decision-relevant information or a general refresher.

On-demand webinars work well for:

- Foundational content that doesn't shift dramatically year-to-year (ALE determination methodology, 1095-C code walkthroughs)

- New hire onboarding for benefits and payroll staff

- Building a reusable internal training library

- Teams in different time zones or with irregular schedules

Live webinars add the most value for:

- Year-end regulatory updates after IRS Q3 guidance drops

- Real-time Q&A on case-specific scenarios (a part-time employee crossing the full-time threshold, a dependent aging off coverage mid-year)

- Q4 benefit design reviews, when affordability thresholds for the upcoming plan year are confirmed

That third live use case has a hard deadline attached. The IRS typically publishes the coming year's affordability percentage in July–September. Rev. Proc. 2025-25, setting the 2026 threshold at 9.96%, came out by late July 2025. Any team finalizing 2026 plan contributions without that number is guessing.

For most teams, the right approach is a hybrid: maintain a core on-demand series for year-round reference and onboarding, then run one or two live sessions timed to IRS guidance releases and filing season preparation, typically September and January.

How to Evaluate and Select an ACA Compliance Webinar Series

Presenter Credentials

Look for:

- ERISA attorneys with IRS correspondence experience. They've seen what actually triggers Letter 226-J.

- Certified Employee Benefit Specialists (CEBS) administered through IFEBP

- Compliance officers from benefits consultancies with hands-on 1094-C/1095-C filing experience

Generalist HR training vendors often produce accessible content. When affordability safe harbor nuances are involved, accessible and accurate aren't the same thing.

Content Currency Check

On-demand series go stale quickly. Outdated content is worse than no training when it teaches the wrong penalty figures or an expired safe harbor percentage. Before enrolling, confirm:

- When was the series last updated?

- Does it reflect the current Rev. Proc. for affordability (9.96% for 2026)?

- Are penalty amounts current ($3,340/$5,010 for 2026)?

- Does it address the mandatory Plan Start Month field?

- Are updates pushed to enrolled users automatically?

Depth vs. Breadth

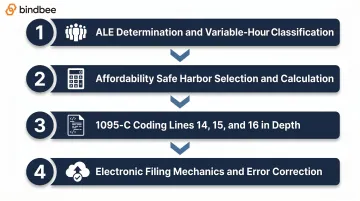

A 10-module survey course covering every ACA topic shallowly often delivers less value than a focused 3–4 module series drilling into:

- ALE determination and variable-hour employee classification

- Affordability safe harbor selection and calculation

- 1095-C coding: Lines 14, 15, and 16 in depth

- Electronic filing mechanics and error correction

A mid-size employer with a large hourly workforce carries different exposure than a fully salaried professional services firm. The right series targets your actual risk areas, not every possible ACA scenario.

Practical Evaluation Criteria

- CE credit eligibility: SHRM PDCs, HRCI recertification credits, or CEBS continuing education

- Supporting materials: Code lookup charts, downloadable checklists, slide decks

- Q&A access: Live help desk or follow-up question capability after completing modules

ACA Certification and Credentials: What They Actually Mean

ACA "certification" is frequently misunderstood. To be direct: there is no federally mandated ACA compliance license. No IRS, DOL, or HHS requirement compels HR staff or benefits administrators to hold a credential to perform compliance functions or file ACA information returns.

What exists are voluntary professional credentials offered by industry associations and training providers:

- NABIP (formerly NAHU): Offers ACA-specific continuing education programs for benefits and insurance professionals

- AHIP: Health insurance certifications with ACA compliance components, primarily for carrier and managed care professionals

- SHRM-CP/SHRM-SCP: ACA compliance webinars may qualify for Professional Development Credits (PDCs) if the provider is SHRM-approved

- HRCI (PHR/SPHR): ACA course content can qualify for recertification credits under Total Rewards or Compliance categories

These credentials signal structured learning and professional commitment to compliance knowledge, not a legal authorization to practice. For HR teams, completing a recognized ACA training series builds internal credibility and supports professional development goals.

For benefits consultants and brokers, the value is external: it shows clients their advisor understands the technical rules, not just the headlines.

Pricing varies widely, from low-cost association webinars to multi-module eLearning programs. Check current pricing directly with NABIP or AHIP.

From Webinar to Action: Operationalizing ACA Compliance in Your Benefits Stack

Training closes the knowledge gap. It doesn't close the data gap. For most organizations, the data gap is where compliance actually breaks down.

Where Errors Actually Originate

The IRS issues Letter 226-J based on discrepancies between employer-filed 1094-C/1095-C data and individual premium tax credit claims. Common triggers:

- Incorrect Line 14 or Line 16 codes — often from not knowing which safe harbor applies to which employee

- Missing offers of coverage for variable-hour employees who crossed the full-time threshold during a measurement period

- Dependent coverage data that doesn't match carrier enrollment records

- Incorrect employee counts or FTE calculations affecting ALE status

The root cause is data integration failure, not gaps in regulatory knowledge.

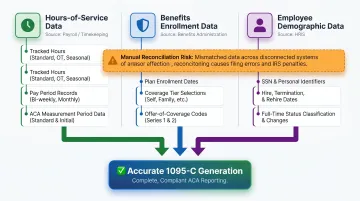

The Three Data Domains ACA Reporting Requires

Accurate 1095-C generation depends on reconciling three separate data streams:

- Hours-of-service data from payroll/timekeeping — for variable-hour employee classification and look-back measurement period calculations

- Benefits enrollment data from benefits administration — plan elections, coverage tiers, effective dates, and dependent relationships

- Employee demographic data from HRIS — employment status, hire dates, job classification, and work location

When these three systems don't talk to each other in real time, reconciliation happens manually, typically in spreadsheets, under deadline pressure, and with predictable gaps in coverage data.

Where Benefits Tech Infrastructure Fits In

For benefits platforms, HR tech vendors, and TPAs building ACA reporting features into their products, the data architecture challenge is as demanding as the compliance knowledge challenge.

Bindbee addresses this directly. Through a single API connected to 65+ HRIS and payroll systems, including Workday, ADP, UKG, Paychex, Gusto, and Rippling, it normalizes the data streams that ACA reporting depends on:

- Employee eligibility status with real-time updates when employment status or hours change in a source system

- Benefits enrollment elections including plan selections, coverage tiers, and effective dates

- Dependent relationships and coverage elections with relationship types, dates of birth, and the effective date fields Form 1095-C Part III requires for self-insured plans

- Hours-worked data for variable-hour employees, with ACA validation across full-time, part-time, and variable-hour classifications

- Webhook notifications triggered when employment status, hours, or dependent enrollment changes upstream

For benefits platforms building ACA compliance features, that normalized data means 1095-C generation logic runs against current, reconciled inputs, not batch files that are weeks out of date.

Frequently Asked Questions

What does it mean to be ACA certified?

ACA certification is a voluntary professional credential awarded by training providers or industry associations like NABIP or AHIP, confirming completion of structured coursework on Affordable Care Act rules. It is not a government-issued license. No federal agency requires it. The credential signals compliance knowledge to employers and clients.

How do I become ACA certified?

Enroll in an ACA-focused course or webinar series from a recognized credentialing body (NABIP, AHIP, or an accredited benefits training provider), complete the required modules or exam, and maintain the credential through periodic continuing education. SHRM and HRCI courses may also count toward existing HR recertification credits.

How much is ACA certification?

Costs vary by provider and program depth, from low-cost association webinars to multi-module eLearning programs. Check current pricing directly with NABIP (nabip.org) or AHIP (ahip.org), as rates and promotional options change regularly.

Is ACA reporting required for 2026?

Yes. ACA reporting obligations under IRC Sections 6055 and 6056 remain fully in effect. For tax year 2025, employers must furnish Form 1095-C to employees by March 2, 2026, and file electronically with the IRS by March 31, 2026 via the IRS AIR system.

What should be included in compliance training?

A complete ACA training program covers ALE determination, Employer Shared Responsibility rules, affordability standards and safe harbors, Form 1095-C indicator codes, and electronic filing requirements. Annual updates on IRS penalty amounts and affordability thresholds should also be included.