The ACA lookback measurement period solves this by tracking each employee's hours over a defined window, typically 12 months, then locking in their coverage status for a subsequent stability period. Get the tracking right, and you have a defensible eligibility record. Get it wrong, and you're looking at IRS Employer Shared Responsibility Payment (ESRP) penalties of up to $4,350 per affected employee in 2025.

This guide is written for HR Tech platforms, benefits administration software, TPAs, and payroll platforms managing ACA compliance workflows on behalf of employers. It covers how the three-period lookback cycle works, what affects tracking accuracy, and where things most commonly break down in practice.

Key Takeaways

- The lookback method is one of two IRS-approved approaches for determining coverage eligibility, best suited for variable-hour workforces.

- It runs in three sequential phases: measurement period, administrative period, and stability period.

- Employees averaging 30+ hours/week or 130+ hours/month during measurement must be offered coverage for the entire stability period, regardless of later hour changes.

- Payroll, HRIS, and benefits data gaps are the most common source of ACA lookback compliance errors.

- For 2025, the Section 4980H(a) "sledgehammer" penalty is $2,900 per full-time employee; the 4980H(b) "shortfall" penalty is $4,350.

What Is the ACA Lookback Measurement Period?

The lookback measurement period is an IRS-sanctioned eligibility-testing window during which an employer tracks each employee's hours of service to calculate their average weekly hours and determine ACA full-time status. Under 26 CFR 54.4980H-3, the period must be no less than 3 and no more than 12 consecutive calendar months, with 12 months being the most common choice in practice.

The result is a stable, defensible record of which employees triggered the employer's obligation to offer minimum essential coverage, and the documented basis for accurate IRS Form 1095-C reporting.

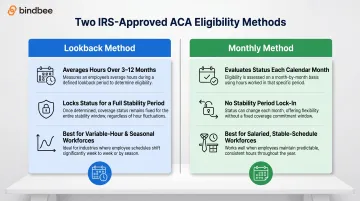

How It Differs from the Monthly Method

The IRS permits two methods for determining full-time status:

| Method | How It Works | Best For |

|---|---|---|

| Lookback | Averages hours over 3–12 months; locks status for a stability period | Variable-hour, seasonal, or fluctuating-schedule workforces |

| Monthly | Evaluates status each calendar month | Predictable, salaried workforces with stable hours |

Employers can apply different methods to different bona fide employee categories. For example, lookback for hourly workers and monthly for salaried employees. Each category must be defined clearly and applied consistently. Shifting employees between methods to avoid coverage obligations creates direct IRS exposure.

Why Applicable Large Employers Use the Lookback Method

Applicable Large Employers (ALEs), employers averaging 50 or more full-time equivalent employees during the prior calendar year, are subject to the ACA employer mandate. Failing to offer affordable minimum essential coverage to full-time employees triggers ESRP penalties under IRC Section 4980H.

For 2025, according to IRS Revenue Procedure 2024-40 reported by Thomson Reuters, those penalties are:

- $2,900 per full-time employee (minus the first 30) for failing to offer coverage to 95%+ of full-time employees, Section 4980H(a)

- $4,350 per full-time employee who receives a premium tax credit (Section 4980H(b)), for coverage that's offered but deemed unaffordable or lacking minimum value

These amounts decreased slightly from 2024, the first reduction since the penalties were indexed for inflation. Don't treat that as a signal of reduced risk. IRS ESRP enforcement has grown more systematic and aggressive, not less.

The Variable-Hour Problem

Industries like hospitality, healthcare staffing, retail, and home care routinely employ workers whose hours swing significantly week to week. Running month-by-month status determinations on these workers creates two concrete problems:

- Recalculating status every month for hundreds of variable-hour employees creates significant administrative overhead

- Workers who log fewer hours in a single month can lose coverage mid-year, even if their average clearly qualifies them as full-time

The lookback method addresses both by averaging hours over a longer window. That average produces a stable status determination that holds for the entire stability period, giving both the employer and employee certainty before the plan year begins.

How the ACA Lookback Measurement Period Works

The lookback process runs in three sequential, non-overlapping phases. These must be applied consistently year over year, and two versions exist: the standard measurement period for existing employees, and the initial measurement period for new variable-hour or seasonal hires. New hires transition to the standard cycle after completing their initial period.

The Standard Measurement Period

This is the hour-tracking phase, typically 12 months, though anywhere from 3 to 12 months is permissible. The math is simple:

Total hours of service ÷ number of weeks in the period = average weekly hours

Any employee averaging 30+ hours/week qualifies as full-time for the subsequent stability period. For a 12-month measurement period, the cumulative threshold works out to 1,560 hours (130 hours × 12 months).

What counts as "hours of service" under IRS regulations at 26 CFR 54.4980H-1(a)(24):

- Every hour an employee is paid or entitled to payment for performing duties

- Every paid hour of non-work time: vacation, holiday, illness, leave of absence, jury duty, military duty, layoff

Two narrow exclusions apply: Federal Work-Study program hours and services by members of religious orders under a vow of poverty. That's it. Paid sick leave counts. Paid holidays count. PTO counts.

For salaried employees where actual hours aren't tracked, the IRS permits equivalency methods: crediting 8 hours per day or 40 hours per week for each day/week with at least one hour of service.

The Administrative Period

Following the measurement period, employers have up to 90 days to complete eligibility calculations, notify employees of their status, and process enrollment before the stability period begins. The administrative period and stability period cannot overlap.

For employees completing an initial 12-month measurement period, the window is tighter. The combined initial measurement period plus administrative period cannot exceed 13 months plus a fraction of a calendar month from the employee's start date. In practical terms, that leaves roughly one month for the administrative phase, not the full 90 days.

The Stability Period

The stability period is when coverage determinations take effect. Key rules:

- Must last at least 6 consecutive calendar months

- Cannot be shorter than the measurement period

- An employee's full-time or part-time status is locked for the entire stability period regardless of actual hours worked

An employee who qualifies as full-time based on the measurement period retains coverage rights for the entire stability period, even if they shift to a part-time role in month 2 of that period. Removing coverage is a direct ESRP penalty trigger.

2025 Form 1095-C deadlines to know:

| Requirement | Deadline |

|---|---|

| Employee furnishing (distribute Form 1095-C) | March 2, 2026 |

| IRS paper filing | March 2, 2026 |

| IRS electronic filing | March 31, 2026 |

Employers filing 10 or more information returns are required to file electronically.

Key Factors That Affect Lookback Measurement Accuracy

Data Integrity Across Systems

ACA lookback compliance is fundamentally a data pipeline problem. Hour records must be complete, month by month, for up to 12 months per employee. Those records live across payroll, HRIS, and benefits systems that often don't talk to each other cleanly.

Disconnected systems create gaps. A payroll system that exports hours weekly and an HRIS that refreshes monthly may produce mismatched records that are nearly impossible to reconcile accurately at the end of a measurement period. As Selerix noted in their analysis of ACA compliance infrastructure, "ACA compliance isn't just a filing task. It's a data problem."

For benefits platforms and HR Tech companies managing ACA workflows at scale, this is where unified employment data infrastructure matters. Bindbee's unified API normalizes hour and employment data from 60+ HRIS and payroll systems including Workday, ADP, Gusto, Paychex, and UKG, through a single integration with automatic incremental syncs. That means measurement period calculations pull from one consistent data source rather than reconciling mismatched exports across systems.

New Hire Tracking Complexity

New variable-hour or seasonal hires require a separate initial measurement period running in parallel with the standard cycle for existing employees. That means tracking two overlapping timelines simultaneously for every recent hire, and ensuring each new hire transitions cleanly to the standard measurement cycle once their initial period ends. Managing that transition is among the most common compliance gaps practitioners identify.

Break-in-Service Rules

The IRS requires employers to account for breaks in service when calculating average hours. The rules differ by employer type:

| Scenario | Break Threshold | Effect |

|---|---|---|

| General employers (break-in-service) | 13 consecutive weeks | Employee treated as rehire; new measurement period begins |

| Educational institutions | 26 consecutive weeks | Accounts for summer/intersession gaps |

| Rule of parity | 4+ weeks AND break exceeds prior employment period | Employer may treat returning worker as a new employee |

Missing these adjustments leads to overstated or understated hour totals, either triggering a coverage obligation that doesn't exist, or missing one that does.

Consistency of Method Application

Employers can apply different measurement methods to different employee categories, but those categories must be bona fide and consistently applied. Permissible distinctions include collectively bargained vs. non-bargained employees, salaried vs. hourly, employees of different entities within a controlled group, and employees in different states.

Reassigning employees between categories to reduce coverage exposure is a known IRS audit trigger. Auditors look at whether category definitions shifted in ways that correlate with benefit eligibility outcomes.

Common Mistakes and Misconceptions

Assuming Salaried Employees Don't Need Measurement

Employees "reasonably expected" to work 30+ hours per week from day one are treated as full-time immediately. They skip the lookback measurement period for initial status. But salaried employees whose hours fluctuate, or who move between roles, still need to go through the standard annual measurement cycle to confirm ongoing ACA status. Pay type is not an exemption.

Removing Coverage During the Stability Period

When a full-time employee shifts to part-time mid-stability period, some employers assume coverage can be adjusted. It can't. Coverage is locked for the full stability period regardless of schedule changes.

The inverse error is equally common: assuming that because someone is no longer working full-time hours, no offer of coverage was required during the stability period at all. Both assumptions expose employers to ACA penalty risk.

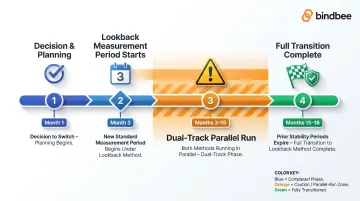

Switching Methods Without Enough Lead Time

Switching from the monthly method to the lookback method isn't a single-cycle change. Per IRS Notice 2014-49, the switch must align with the start of a new standard measurement period. Employees already in a stability period retain their locked status until that period ends.

In practice, transitions require 12 to 18 months of planning. Historical data must accumulate under the new method while the prior method stays in effect, meaning both systems run in parallel for an extended stretch.

Frequently Asked Questions

How do you determine ACA measurement periods?

Employers choose any consistent start date for a standard measurement period of 3 to 12 months. 12 months is the most common. The period should align with the plan year and use whole months. The same period must be applied consistently to all employees in the same category, year over year.

How are hours calculated for ACA purposes?

Total hours of service during the measurement period are divided by the number of weeks to determine average weekly hours. An average of 30 or more hours per week (or 130+ hours per month) means the employee is ACA full-time. All paid hours count, including paid leave, with two exceptions: Federal Work-Study participants and members of religious orders under a vow of poverty.

What does the ACA stability period mean?

The stability period is the window, at least 6 months and typically 12, during which an employee's coverage status is locked based on their measurement period outcome. An employee who qualified as full-time retains coverage rights for the entire stability period even if their hours drop, and removing that coverage creates ESRP penalty exposure.

Is it legal to track hours for salaried employees?

Yes. Tracking hours for ACA purposes is legally permissible for salaried employees and does not conflict with FLSA exempt status. The two frameworks operate independently. Where time records aren't kept, the IRS permits equivalency methods (8 hours/day or 40 hours/week) as a compliant alternative.

Does PTO count as hours worked for ACA?

Yes. Paid time off, including vacation, sick leave, holidays, and any other employer-paid periods of non-work, counts as hours of service under the IRS definition. The standard covers any hour for which an employee is paid or entitled to payment, regardless of whether actual work was performed.